Mutual Funds: Different Types and How They Are Priced

What Is a Mutual Fund?

A mutual fund is one where money from many people is pooled together to invest in a diversified array of stocks, bonds, or other securities. This investment mix is taken care of by a professional money manager, thus giving individuals a portfolio that is structured to match the investment objectives stated in its prospectus.

By investing in a mutual fund, one gets to diversify investments in many different areas, which would reduce risk compared to putting all money into a single stock or bond. Investors make profits or returns on the performances of the fund after deducting any charges or fees. In this way, mutual funds allow small investors or even individual investors to access professionally managed portfolios of equities, bonds, and other classes of assets.1

Key Takeaways

- A mutual fund is a type of investment vehicle consisting of a portfolio of stocks, bonds, or other securities.

- Mutual funds give small or individual investors access to diversified, professionally managed portfolios.

- Mutual funds are divided into several kinds of categories, representing the kinds of securities they invest in, their investment objectives, and the type of returns they seek.

- Mutual funds charge annual fees, expense ratios, or commissions, which may affect their overall returns.

- Employer-sponsored retirement plans commonly invest in mutual funds.

Understanding Mutual Funds

A mutual fund is an investment in which money is pooled from many people and then invested in a variety of assets, such as stocks, bonds, or other securities. That pooling of money allows individuals to diversify their investments and access a greater range of strategies or assets than they might be able to alone.

A mutual fund effectively owns a portfolio of investments that is funded by all the investors who have purchased shares in the fund. So when an individual buys into a mutual fund, they gain part-ownership of all the underlying assets that fund owns. This gives the individual investor exposure to a much wider swath of the market through a single mutual fund investment compared to what they might be able to buy individually.

The performance of the mutual fund depends on the underlying assets that it holds. If these assets increase in value on net, so does the value of the fund's shares. Conversely, if the assets decrease in value, so does the value of the shares.

The fund manager manages the portfolio, deciding how to invest the money across sectors, industries, companies, etc., based on the declared strategy of the fund. Pooling money into a large fund allows individual investors to take part in a professionally managed diversified portfolio of securities that they otherwise wouldn't be able to, given their normal investment amounts. This diversification and access are a key benefit for individual investors looking at mutual funds.

How Are Returns Calculated for Mutual Funds?

Investors typically earn a return from a mutual fund in three ways:

- Income is earned from dividends on stocks and interest on bonds held in the fund's portfolio, and it pays out nearly all of the income it receives over the year to fund owners in the form of a distribution. Funds often give investors a choice either to receive a check for distributions or to reinvest the earnings to purchase additional shares of the mutual fund.

- Portfolio Distributions: If the fund sells securities that have increased in price, the fund realizes a capital gain, which most funds also pass on to investors in a distribution.

- Capital Gains: When the fund's shares increase in price, you can sell your mutual fund shares for a profit in the market.

When an investor researches the returns of a mutual fund, he or she will generally come across "total return," or the net change in value, either up or down, of an investment over a given period. It includes any interest, dividends, or capital gains the fund generated as well as the change in its market value over some time. Total returns are typically calculated over periods of one year, five years, and ten years, as well as from the date the fund was first launched (its inception date).

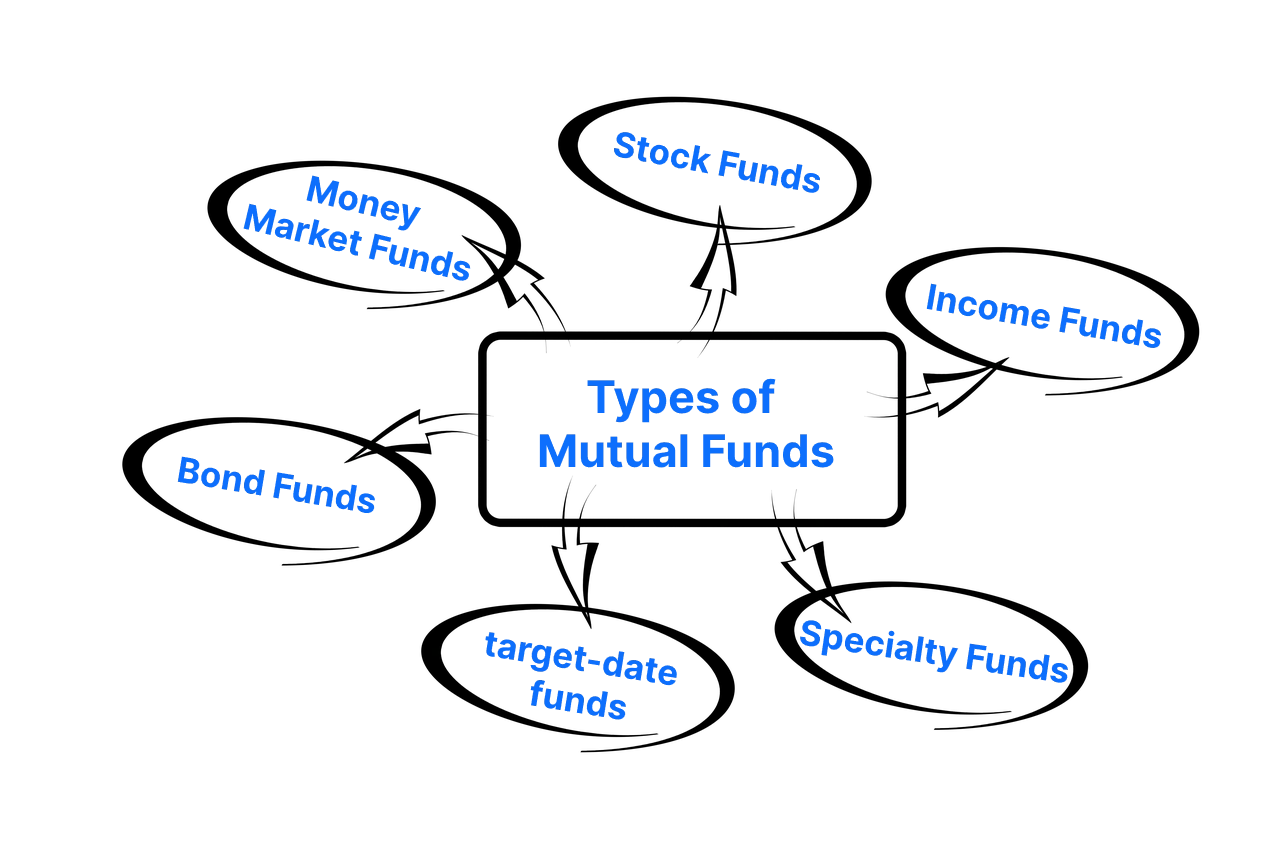

Types of Mutual Funds

There are several types of mutual funds available for investment, though most mutual funds fall into one of four main categories which include stock funds, money market funds, bond funds, and target-date funds.

Stock Funds

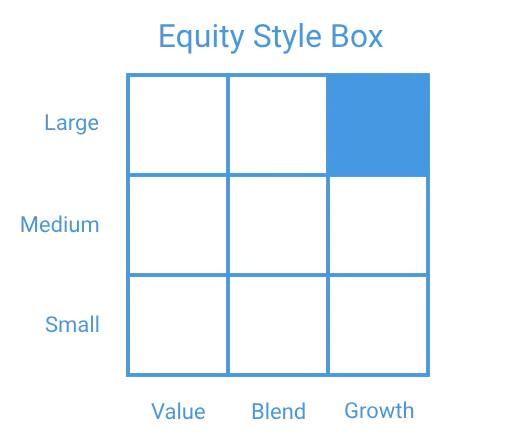

As the name suggests, this fund primarily invests in equities or stocks. Within this category, there are several subcategories. Some equity funds are classified based on the size of the companies they target: small-cap, mid-cap, or large-cap. Others are identified by their investment strategy, such as aggressive growth, income-oriented, or value. Additionally, equity funds can be categorized based on whether they focus on domestic (U.S.) stocks or international equities. To grasp the range of equity funds, you can refer to a style box, an example of which is provided below.

Funds can be categorized based on the size of the companies, their market capitalizations, and the growth potential of the stocks they invest in. A value fund is a type of investment strategy that seeks out high-quality, low-growth companies that are currently out of favor in the market. These companies often have low price-to-earnings (P/E) ratios, low price-to-book (P/B) ratios, and offer dividend yields. On the other hand, growth funds target companies that exhibit strong growth in earnings, sales, and cash flow. These companies usually have high P/E ratios and typically do not distribute dividends. A middle ground between strict value and growth investing is known as a "blend," which includes companies that do not fit neatly into either category and are considered to be in between.

Large-cap companies are characterized by their significant market capitalizations, typically exceeding $10 billion. The market cap is calculated by multiplying the share price by the total number of shares outstanding. Large-cap stocks are usually well-known blue-chip firms. On the other hand, small-cap stocks have market capitalizations between $250 million and $2 billion, often representing newer and riskier investment opportunities. Mid-cap stocks serve as a bridge between small-cap and large-cap categories.

A mutual fund can combine different strategies based on investment style and company size. For instance, a large-cap value fund targets large-cap companies that are financially stable but have recently experienced a decline in their share prices, positioning it in the upper left quadrant of the style box (large and value). Conversely, a fund that focuses on startup technology companies with promising growth potential would be categorized as small-cap growth. This type of mutual fund would be located in the bottom right quadrant (small and growth).

What are large-cap stocks?

Large-cap companies are established businesses that command a significant market share, typically with market caps of ₹20,000 crore or more. These firms are industry leaders and tend to be very stable, often weathering recessions and other challenging situations effectively. Many of them have been in operation for decades and have built a solid reputation. Investing in large-cap stocks is a good choice for those looking to minimize risk. These stocks are generally less volatile compared to mid-cap and small-cap stocks, which contributes to their lower risk profile. However, this lower risk often means that the potential returns may also be less than those offered by mid and small-cap stocks.

What are mid-cap stocks?

Mid-cap companies are those with market capitalizations ranging from ₹5,000 crore to ₹20,000 crore. Investing in these firms can carry more risk compared to large-cap companies, as mid-caps often experience greater volatility. However, they also have the potential to grow into large-cap companies over time. This growth potential makes mid-cap stocks appealing to many investors.

What are small-cap stocks?

Small-cap companies are defined as those with a market capitalisation of under ₹5,000 crores. These firms tend to be smaller and possess considerable growth potential. However, they also carry a higher risk due to their lower likelihood of long-term success, which contributes to the volatility of their stocks. Historically, small-cap companies have struggled to perform well, but during periods of economic recovery, their stocks frequently emerge as top performers.

Bond Funds

A mutual fund that guarantees a minimum return falls under the fixed income category. These funds primarily invest in assets that provide a consistent rate of return, including government bonds, corporate bonds, and various debt instruments. The interest income generated by the fund's portfolio is distributed to the shareholders.

Often called bond funds, these investment vehicles are typically actively managed and aim to purchase bonds that are considered undervalued, with the intention of selling them for a profit. While these mutual funds may offer higher returns, they also come with risks. For instance, a fund that focuses on high-yield junk bonds carries significantly more risk compared to one that invests in government securities.

Because there are many different types of bonds, bond funds can vary dramatically depending on where they invest, and all bond funds are subject to interest rate risk.

Index Funds

Index funds invest in stocks that track major market indices like the S&P 500 or the Dow Jones Industrial Average (DJIA). This approach demands less research from analysts and advisors, which means lower costs for shareholders. As a result, these funds are typically tailored for cost-conscious investors.

Balanced Funds

Balanced funds invest in a mix of asset classes, including stocks, bonds, money market instruments, and alternative investments. The goal of this type of fund, often referred to as an asset allocation fund, is to minimize risk by diversifying across different asset classes.

Some funds are designed with a fixed allocation strategy, allowing investors to have a consistent exposure to different asset classes. In contrast, other funds adopt a dynamic allocation strategy that adjusts percentages to align with various investor goals. This approach can involve reacting to market trends, shifts in the business cycle, or the evolving stages of the investor's life.

The portfolio manager is commonly given the freedom to switch the ratio of asset classes as needed to maintain the integrity of the fund's stated strategy.

Money Market Funds

The money market is made up of secure, low-risk, short-term debt instruments, primarily government Treasury bills. While investors may not see significant returns, their principal is assured. Typically, the returns are slightly higher than what one would earn in a standard checking or savings account, but a bit lower than the average certificate of deposit (CD).

Income Funds

Income funds are designed to deliver consistent income over time. They mainly invest in government bonds and high-quality corporate debt, holding these bonds until they mature to generate interest payments. Although the value of the fund's holdings may increase, the main goal is to ensure a reliable cash flow for investors. Consequently, these funds typically attract conservative investors and retirees.

International/Global Funds

An international fund, also known as a foreign fund, focuses solely on assets situated outside the investor's home country. In contrast, global funds have the flexibility to invest in markets worldwide. The volatility of these funds is often influenced by the specific economic and political risks of the countries in which they invest. Nevertheless, incorporating these funds into a well-balanced portfolio can enhance diversification, as returns from foreign markets may not always align with those from the investor's home market.

Specialty Funds

Sector funds are specialized investment funds that focus on particular sectors of the economy, like financial services, technology, or healthcare. These funds can experience significant volatility because the stocks within a specific sector often move in tandem with one another.

Regional funds simplify the process of concentrating on a particular geographic area. This could involve targeting a larger region or honing in on a single country.

Socially responsible funds, also known as ethical funds, focus their investments on companies that align with specific guidelines or values. For instance, many socially responsible funds avoid investing in "sin" industries like tobacco, alcohol, weapons, or nuclear energy. Conversely, some funds concentrate on green technologies, including solar and wind energy or recycling initiatives.

Mutual Fund Fees

A mutual fund incurs annual operating fees or shareholder fees. These fees are typically a small percentage of the total funds under management, usually less than 1%, and are referred to as the expense ratio. The expense ratio of a fund includes both the advisory or management fee and its administrative costs.

Shareholder fees include sales charges, commissions, and redemption fees that investors pay directly when they buy or sell funds. Sales charges or commissions are commonly referred to as "the load" of a mutual fund. If a mutual fund has a front-end load, fees are charged at the time of purchase. Conversely, with a back-end load, fees are applied when investors sell their shares.

Sometimes, an investment company may provide a no-load mutual fund, which means there are no commissions or sales charges involved. These funds are sold directly by the investment company instead of going through a third party. Additionally, some funds may impose fees or penalties for early withdrawals or for selling the investment before a certain period has passed.

Classes of Mutual Fund Shares

Typically, individual investors buy mutual funds with A-shares via a broker. This purchase often comes with a front-end load that can reach 5% or more, in addition to management fees and ongoing distribution fees, referred to as 12b-1 fees. Financial advisors promoting these products might urge clients to opt for higher-load options to earn commissions. With front-end funds, investors incur these costs at the time of their investment in the fund.

To address these issues and comply with fiduciary-rule standards, investment companies have introduced new share classes, such as "level load" C shares. These shares typically do not have a front-end load but do include an annual 12b-1 distribution fee that can be as high as 1%.

Funds that charge management and other fees when an investor sells their holdings are classified as Class B shares.

How To Invest in Mutual Funds

Investing in mutual funds is a fairly straightforward process that involves the following steps:

- Make sure you have a brokerage account with enough cash on hand, and with access to mutual fund shares.

- Identify specific mutual funds that align with your investment goals regarding risk, returns, fees, and minimum investments. Numerous platforms provide tools for screening and researching funds.

- Decide how much you want to invest at the start and place your trade. If you prefer, you can usually set up automatic recurring investments as you wish.

- Monitor and review performances periodically, making adjustments as needed.

- When it is time to close your position, enter a sell order on your platform.

How Mutual Fund Shares Are Priced

The value of a mutual fund is determined by how well the securities within it perform. When an investor purchases a unit or share of a mutual fund, they are essentially buying a portion of its portfolio's performance or, more specifically, a fraction of its overall value. Investing in mutual fund shares is different from investing in individual stock shares. Unlike stocks, mutual fund shares do not provide holders with voting rights. A share in a mutual fund represents investments across a variety of stocks or other securities.

The price of a mutual fund share is known as the net asset value (NAV) per share, which is sometimes abbreviated as NAVPS. To calculate a fund's NAV, you divide the total value of the securities in the portfolio by the total number of shares that are outstanding. Outstanding shares include those held by all shareholders, institutional investors, and company officers or insiders.

Mutual fund shares are usually bought or sold at the fund's current net asset value (NAV), which remains stable during market hours and is finalized at the end of each trading day. The price of a mutual fund is also adjusted when the NAV per share (NAVPS) is determined.

A typical mutual fund consists of a variety of securities, providing shareholders with diversification. For instance, think about an investor who only purchases Google stock and depends solely on the company's performance. Since all their investment is concentrated in one company, their financial outcomes hinge entirely on its success. In contrast, a mutual fund might include Google among its holdings, allowing the performance of other companies in the fund to balance out the fluctuations of a single stock.

Pros and Cons of Mutual Fund Investing

There are several reasons why mutual funds have become the preferred investment option for retail investors, with a significant portion of funds in employer-sponsored retirement plans allocated to mutual funds.

Pros

- Liquidity

- Diversification

- Minimal investment requirements

- Professional management

- Variety of offerings

Cons

- High fees, commissions, and other expenses

- Large cash presence in portfolios

- No FDIC coverage

- Difficulty in comparing funds

- Lack of transparency in holdings

Pros of Mutual Fund Investing

Pros of Mutual Fund Investing

Diversification, which involves mixing various investments and assets in a portfolio to minimize risk, is a key benefit of investing in mutual funds. A well-diversified portfolio includes securities from different industries and capitalizations, as well as bonds with a range of maturities and issuers. Mutual funds can provide diversification more quickly and cost-effectively than purchasing individual securities.

Easy Access

Mutual funds can be easily bought and sold on major stock exchanges, which makes them highly liquid investments. Additionally, for certain asset types, such as foreign equities or exotic commodities, mutual funds are often the most practical option—sometimes the only option—for individual investors to get involved.

Economies of Scale

Mutual funds offer economies of scale by eliminating many commission fees, which helps in building a diversified portfolio. Purchasing individual securities one at a time can result in significant transaction costs. The lower investment amounts in mutual funds enable investors to benefit from dollar-cost averaging.

Since a mutual fund trades in large volumes of securities, it benefits from lower transaction costs compared to what an individual investor would incur. This allows a mutual fund to invest in specific assets or take larger positions than a smaller investor could manage.

Professional Management

A professional investment manager relies on thorough research and adept trading strategies. For small investors, a mutual fund offers an affordable option to have a dedicated manager who handles and oversees their investments. With significantly lower investment minimums, mutual funds present a cost-effective opportunity for individual investors to access and gain from professional money management.

Professional Management

Investors have the flexibility to explore and choose from a range of managers who employ different styles and management objectives. A fund manager might concentrate on value investing, growth investing, developed markets, emerging markets, income generation, or macroeconomic strategies, among various other approaches. This diversity enables investors to access not just stocks and bonds, but also commodities, international assets, and real estate through specialized mutual funds. Mutual funds offer avenues for both foreign and domestic investments that might not be readily available to typical investors.

Mutual funds are subject to industry regulation that ensures accountability and fairness to investors.

Cons of Mutual Fund Investing

Liquidity, diversification, and professional management all make mutual funds attractive options; however, mutual funds have drawbacks too.

No Guarantees

As with many investments that don't come with a guaranteed return, there's always a chance that the value of your mutual fund could decrease. Equity mutual funds are subject to price changes, just like the stocks within the fund's portfolio. It's important to note that mutual fund investments are not insured by the Federal Deposit Insurance Corporation (FDIC).

Cash Drag

Mutual funds need to keep a substantial portion of their portfolios in cash to handle daily share redemptions. To ensure they have enough liquidity for withdrawals, these funds usually hold more cash than an average investor would. Since cash doesn't generate any returns, it's commonly known as "cash drag."

High Costs

Mutual funds offer investors the benefit of professional management, but they also come with fees that can diminish the overall returns for investors, regardless of how well the fund performs. Because these fees can differ significantly from one fund to another, overlooking them can lead to unfavorable long-term effects, especially since actively managed funds face transaction costs that build up over time.

Diworsification" and Dilution

"Diworsification"—a clever twist on words—refers to an investment or portfolio strategy suggesting that excessive complexity can yield poorer outcomes. Many mutual fund investors often make things more complicated than necessary. They tend to buy too many funds that are closely related, which ultimately diminishes the advantages of diversification.

Dilution can also occur when a successful fund becomes too large. When new investments flow into funds with strong performance histories, the manager may struggle to identify appropriate opportunities for all the additional capital to be effectively utilized.

The Securities and Exchange Commission (SEC) mandates that funds must invest at least 80% of their assets in the specific type of investment indicated by their names. How the remaining assets are allocated is at the discretion of the fund manager. However, the categories that qualify for this 80% can be somewhat ambiguous and broad. This allows a fund to potentially mislead prospective investors through its name. For instance, a fund that primarily invests in Argentinian stocks might be marketed under a more general title like "International High-Tech Fund."

End-of-Day Trading Only

A mutual fund lets you convert your shares into cash whenever you want. However, unlike stocks that can be traded throughout the day, most mutual fund redemptions occur only at the end of each trading day.

Taxes

When a fund manager sells a security, it triggers a capital-gains tax. However, taxes can be reduced by investing in tax-sensitive funds or by keeping non-tax-sensitive mutual funds in a tax-deferred account, like a 401(k) or IRA.

Evaluating Funds

Researching and comparing funds can be quite challenging. Unlike stocks, mutual funds don't provide investors with the ability to directly compare metrics like the price to earnings (P/E) ratio, sales growth, earnings per share (EPS), or other key data. While a mutual fund's net asset value can serve as a point of reference, the variety of portfolios makes it tough to make direct comparisons, even among funds that have similar names or objectives. Typically, only index funds that track the same markets are truly comparable.

Example of a Mutual Fund

One of the most prominent mutual funds is Fidelity Investments' Magellan Fund (FMAGX). Launched in 1963, the fund aimed for capital appreciation through investments in common stocks. Its peak success occurred from 1977 to 1990, during which Peter Lynch was the portfolio manager. Under Lynch's leadership, the assets managed by Magellan skyrocketed from $18 million to $14 billion.

Fidelity's performance remained robust, with assets under management (AUM) reaching almost $110 billion by 2000. By 1997, the fund had grown so large that Fidelity decided to close it to new investors, not reopening it until 2008.22

As of February 2023, Fidelity Magellan has around $30 billion in assets and has been under the management of Sammy Simnegar since February 2019. The fund primarily uses the S&P 500 as its benchmark.

Mutual Funds vs. Index Funds

Index funds are a kind of mutual fund designed to match the performance of a specific market benchmark, or index. For instance, an S&P 500 index fund follows that index by investing in the 500 companies in the same proportions as the index itself. One of the main objectives of index funds is to keep costs low in order to closely reflect their index.

In contrast, actively managed mutual funds aim to outperform the market by selecting specific stocks and adjusting their allocations. The fund manager makes decisions based on their investment strategy and research to achieve returns that exceed a benchmark.

| Index vs. Active Mutual Funds |

| Attribute |

Index Funds |

Active Funds |

| Goal |

Match a market index |

Outperform the market |

| Management Style |

Passive, automated |

Active by fund managers |

| Fees |

Low expense ratios |

Higher expense ratios |

| Performance |

Average market returns |

Attempt to beat averages |

Index funds offer market returns at lower costs, while active mutual funds aim for higher returns through skilled management that often comes at a higher price. Investors should consider costs, time horizons, and risk appetite when deciding between index or managed mutual fund investing.